Master Your Wealth: The Ultimate Guide to Compound Interest

Albert Einstein reputedly called it the “eighth wonder of the world.” Financial wizards swear by it. It is the simple mathematical principle that turns modest savings into massive fortunes over time. We are talking about compound interest.

If you have ever wondered how early retirees build their nest eggs or how savvy investors seem to multiply their money effortlessly, the answer often lies in the magic of compounding. But you don’t need a degree in finance to make it work for you. With the right knowledge and tools—like our Compound Interest Calculator—you can map out a clearer path to financial freedom.

In this guide, we will break down exactly what compound interest is, how to use our calculator to project your earnings, and actionable strategies to maximize your returns.

Initial Investment ($)

Annual Interest Rate (%)

Time (Years)

What Is Compound Interest? (And Why You Should Care)

At its core, interest is the cost of using money. When you borrow money, you pay interest. When you lend money (like depositing it in a savings account or investing it), you earn interest.

There are two main types of interest: simple and compound.

- Simple Interest is calculated only on the principal amount (the initial money you put in). If you invest $1,000 at 5% simple interest, you earn $50 every year. After 10 years, you have earned $500 in total interest.

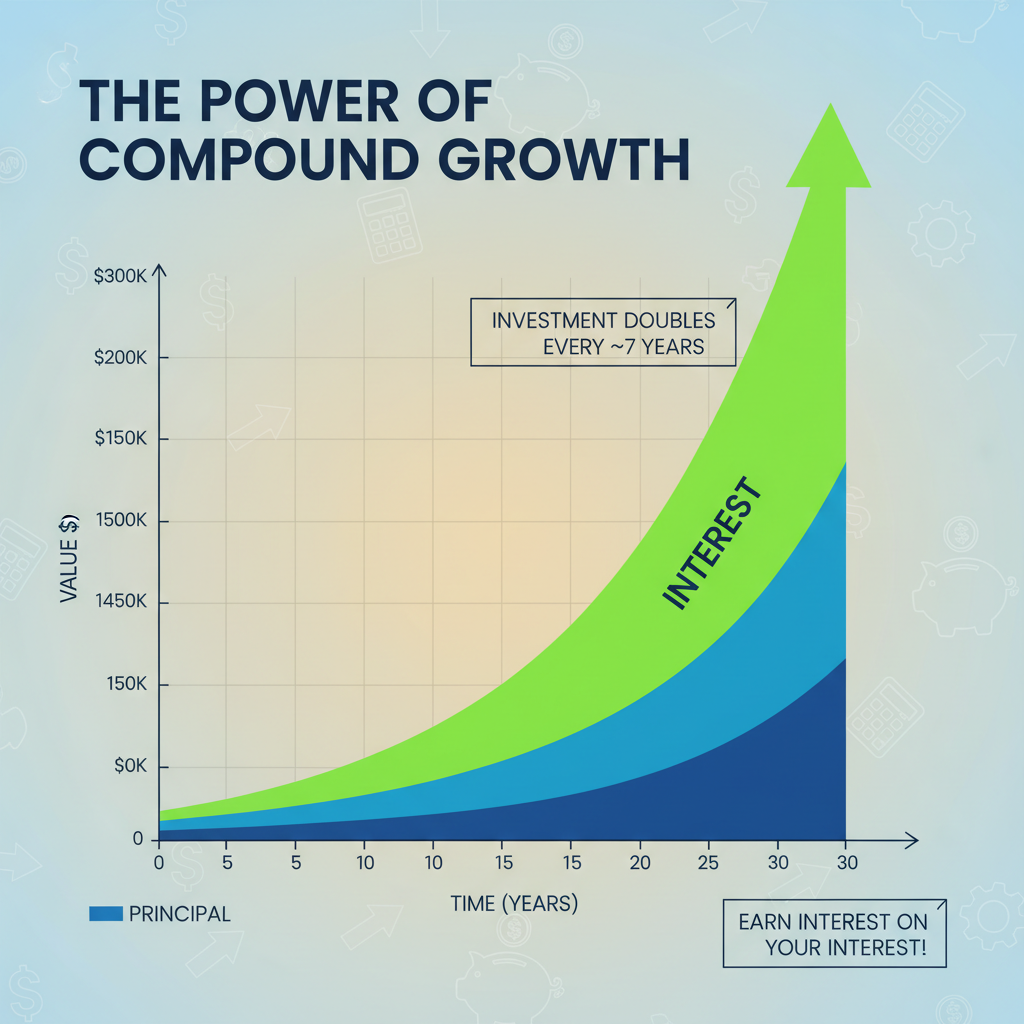

- Compound Interest is where the magic happens. It is interest calculated on the initial principal plus all the accumulated interest from previous periods. You earn interest on your interest.

The Snowball Effect

Imagine rolling a small snowball down a snowy hill. As it rolls, it picks up more snow. The larger the surface area of the snowball, the more snow it picks up with every turn. By the time it reaches the bottom, that tiny snowball has become a massive boulder.

That is compound interest. Your money grows faster as time goes on because the base amount—your principal plus earned interest—keeps getting bigger.

How to Use the Thinkfixer Compound Interest Calculator

We designed our Compound Interest Calculator to be intuitive and powerful. You don’t need to mess around with complex spreadsheets or formulas. Here is a step-by-step guide to projecting your future wealth.

Step 1: Enter Your Initial Investment

This is your starting point. How much money do you have ready to invest right now? This could be the $500 in your savings account or a $10,000 inheritance.

- Input: Enter the dollar amount in the Initial Investment ($) field.

Step 2: Determine Your Annual Interest Rate

This is the percentage return you expect to earn on your money each year.

- Savings Accounts: Typically offer 0.5% to 5% (high-yield accounts).

- Stock Market (S&P 500): Historically averages around 7% to 10% annually after inflation.

- Real Estate: Returns vary widely but often range between 8% and 12%.

- Input: Enter the percentage in the Annual Interest Rate (%) field.

Step 3: Set Your Time Horizon

How long do you plan to let this money grow? Time is the most critical factor in compounding. The longer you leave the money untouched, the more dramatic the growth.

- Input: Enter the number of years in the Time (Years) field.

Step 4: Analyze the Results

Click Calculate. You will instantly see a projection of your total balance. Compare this final number to your initial investment to see exactly how much “free money” your patience has earned you.

Example Scenario:

Let’s say you invest $5,000 today.

- Interest Rate: 8%

- Time: 20 years

Without adding another penny, that $5,000 would grow to approximately $23,304. That is over $18,000 in pure profit, just for waiting!

The Wealth-Building Benefits of Compound Interest

Why do financial experts obsess over this concept? Because it changes the way you approach saving. It shifts your mindset from “saving leftovers” to “building a money machine.”

1. Your Money Works for You

The hardest money to earn is your paycheck because you trade your time for it. Investment returns are different. Your money works 24/7, never takes a sick day, and keeps growing even while you sleep. Compound interest accelerates this passive income generation.

2. It Rewards Patience, Not Just Capital

You do not need to be rich to get rich. Time can often outweigh capital. A young person investing small amounts often ends up wealthier than a high earner who starts investing late. This levels the playing field, making wealth accessible to anyone with discipline.

3. Protection Against Inflation

Inflation erodes the purchasing power of your cash. A dollar today buys less than a dollar ten years ago. By utilizing compound interest in investment vehicles that outpace inflation (like stocks or real estate), you ensure your future self can afford the same lifestyle you enjoy today.

Real-Life Applications: When to Use This Calculator

Compound interest isn’t just an abstract math concept; it applies to almost every major financial goal.

Retirement Planning

This is the most common use case. If you are 30 years old and want to retire at 65, you have 35 years of compounding ahead of you. Using the calculator allows you to see if your current savings are on track to support your retirement lifestyle. If the numbers look low, you know immediately that you need to either increase your initial investment or find a higher interest rate.

Education Funds

College is expensive, and tuition costs are rising. Parents often start “529 plans” or education savings accounts when a child is born. By investing early, the compound interest covers a significant chunk of the tuition bill, reducing the burden of student loans later.

Down Payments for Homes

Saving for a house can feel daunting. Parking your down payment fund in a high-yield savings account or a conservative investment portfolio can help you reach your target faster than using a standard checking account.

Strategies to Maximize Your Returns

Now that you understand the mechanics, how do you supercharge the results? Here are three proven strategies.

1. Start Early (The Time Factor)

We cannot stress this enough: Time is your best friend.

Consider two investors, Jack and Jill.

- Jack invests $200/month from age 25 to 35, then stops completely.

- Jill waits until age 35 to start, then invests $200/month until age 65.

Even though Jill invests for 30 years and Jack only invested for 10, Jack often ends up with more money simply because his money had an extra 10 years to compound. Do not wait for the “perfect time” to start. Start now.

2. Reinvest Your Dividends

If you invest in stocks that pay dividends (a share of company profits), do not spend that cash. Reinvest it to buy more shares. Those new shares will pay their own dividends, which buys even more shares. This creates a powerful feedback loop that accelerates compounding.

3. Minimize Fees

Investment fees are the enemy of compound interest. A 1% management fee might sound small, but over 30 years, it can eat up tens of thousands of dollars of your potential growth. Look for low-cost index funds or ETFs (Exchange Traded Funds) to keep more of your money working for you.

Related Tools for Financial Success

While the Compound Interest Calculator is powerful, it is just one piece of the puzzle. To build a comprehensive financial plan, explore our other tools:

Savings Calculator

While similar, a savings calculator is often better suited for shorter-term goals or accounts with regular monthly contributions. Use this if you plan to add money to your pot every month rather than just letting a lump sum sit.

Passive Income Calculator

Once you have built up a nest egg using compound interest, you might want to live off the returns. The Passive Income Calculator helps you determine how much monthly income your investments can generate without depleting the principal.

Frequently Asked Questions (FAQs)

Q: Does the calculator account for inflation?

A: No, this is a nominal return calculator. To account for inflation, you should subtract the expected inflation rate (usually 2-3%) from your expected interest rate. For example, if you expect an 8% return and 3% inflation, enter 5% into the calculator for a “real return” estimate.

Q: What is a realistic interest rate to use?

A: It depends on your risk tolerance.

- Conservative: 3-4% (Bonds, High-Yield Savings)

- Moderate: 5-7% (Balanced Portfolio)

- Aggressive: 8-10% (Stock Market Index Funds)

Q: Can I lose money while trying to earn compound interest?

A: Yes, if you invest in assets like stocks or cryptocurrency, the value can go down. Compound interest works best over long periods where market volatility smooths out. Savings accounts are safer but offer lower returns.

Q: How often is interest compounded in this calculator?

A: Our standard calculator assumes annual compounding. In reality, some accounts compound monthly or daily, which would result in slightly higher returns than shown here.

Conclusion

Compound interest is the engine of wealth creation. It is fair, mathematical, and predictable. By understanding how it works and using tools like the Thinkfixer Compound Interest Calculator, you take control of your financial destiny.

Remember, the best day to start investing was yesterday. The second best day is today. Plug your numbers into the calculator above and see what your future could look like.

To better understand how compound interest works, you can explore this compound interest explanation by Investor.gov.