Warrant in Debt: What It Means and What to Do If You Receive One (2026 Guide)

Have you ever opened your mailbox, pulled out an official-looking envelope, and felt your stomach instantly drop? Many people completely panic when they receive a warrant in debt! It sounds absolutely terrifying, almost like an arrest warrant that will have the police knocking on your door. But take a deep breath—it is not an arrest warrant!

If you are holding one of these papers right now, it simply means someone is suing you for money. While it is a serious financial matter, knowing exactly what to do can save your credit, your bank account, and your peace of mind! Let’s walk through everything you need to know about this document so you can tackle it with total confidence.

What Is a Warrant in Debt? (Quick Answer)

A warrant in debt is a legal document issued by a court notifying someone that they are being sued for unpaid debt. It is not an arrest warrant but a civil lawsuit requesting payment.

What to Do Immediately After Receiving a Warrant in Debt

Stay calm and read the document carefully

Check the court date

Verify the debt amount

Start gathering documents

Consider contacting the creditor

Who Can Issue a Warrant in Debt?

Credit card companies

Debt collectors

Landlords

Medical providers

Personal lenders

Where Is a Warrant in Debt Common?

Virginia (Most popular search)

Maryland

Washington DC

Small claims courts

What Is a Warrant in Debt?

Let’s break down the what is a warrant in debt question into bite-sized pieces! A warrant in debt is simply a legal document used in local civil courts (like a warrant in debt Virginia court) to officially notify you that a person or company is suing you for an unpaid debt.

In plain English? The warrant in debt meaning is just “a claim for money.” A judge or court clerk issues this document after a creditor files a lawsuit against you. It happens when a creditor believes you owe them money and they want the court to step in and force you to pay.

Think of it like a referee blowing a whistle in a sports game. The creditor is telling the referee (the court) that you broke the rules by not paying, and they want the referee to make a call!

According to the Consumer Financial Protection Bureau, debt collection lawsuits are increasingly common as creditors pursue unpaid balances through the legal system.

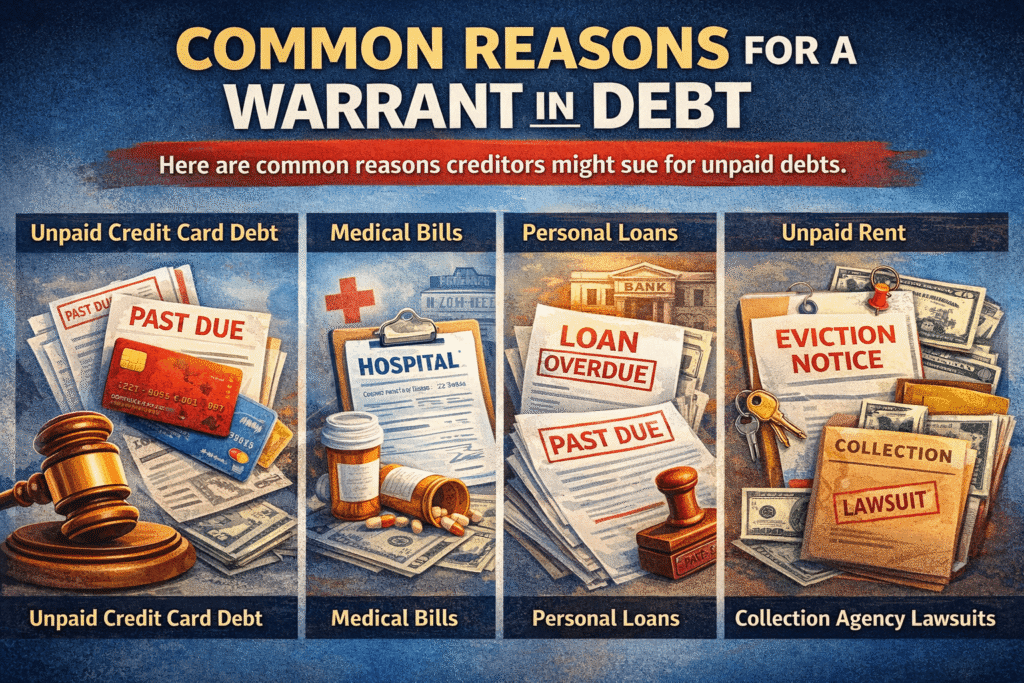

Why Would You Receive a Warrant in Debt?

People receive these notices for all sorts of everyday financial reasons. Sometimes, we fall on hard times, and bills pile up! Let’s look at the most common reasons you might find this document in your hands.

Unpaid Credit Card Debt

Credit cards are helpful, but balances can quickly spiral out of control. If you stop making payments for several months, the credit card company might decide to take legal action to get their money back.

Medical Bills

Medical emergencies are incredibly stressful, and the massive bills that follow are even worse! Hospitals and doctors’ offices often use courts to collect unpaid medical debts if you cannot cover the costs.

Personal Loans

Borrowing money from a bank or lender comes with a strict repayment contract. If you default on a personal loan, especially if you had to seek no credit financing options, the lender will likely send a warrant in debt to collect the remaining balance. The same goes for vehicle agreements; even bad credit leasing contracts can lead to legal action if the payments suddenly stop.

Unpaid Rent

If you fall behind on rent after moving out, your former landlord can use this process to sue you for the back rent or damages to the apartment.

Collection Agency Lawsuits

Often, your original creditor will sell your debt to a third-party debt collector. These collection agencies are very aggressive and frequently use the warrant in debt court process to demand payment.

What Happens After You Receive a Warrant in Debt?

Knowing what happens next takes the mystery and fear out of the process! Here is exactly what you can expect:

You Receive Court Notice

The first step is receiving the physical paper, often called a warrant in debt form. It might be handed to you by a sheriff, mailed to your house, or even taped to your front door!

Court Date Scheduled

Look closely at the document! It will have a specific date and time printed on it. This is your “return date” or your first court appearance.

You Must Respond

You cannot just ignore it! Learning how to respond to warrant in debt notices is crucial. You usually have to show up on that court date or file a written answer with the court to say whether you agree or disagree that you owe the money.

Judge Makes Decision

During the hearing, the judge will listen to both sides. The creditor must prove you owe the money, and you get a chance to defend yourself!

Possible Judgment

If the judge agrees with the creditor, they will issue a “judgment” against you. This is an official court order stating you legally owe the debt.

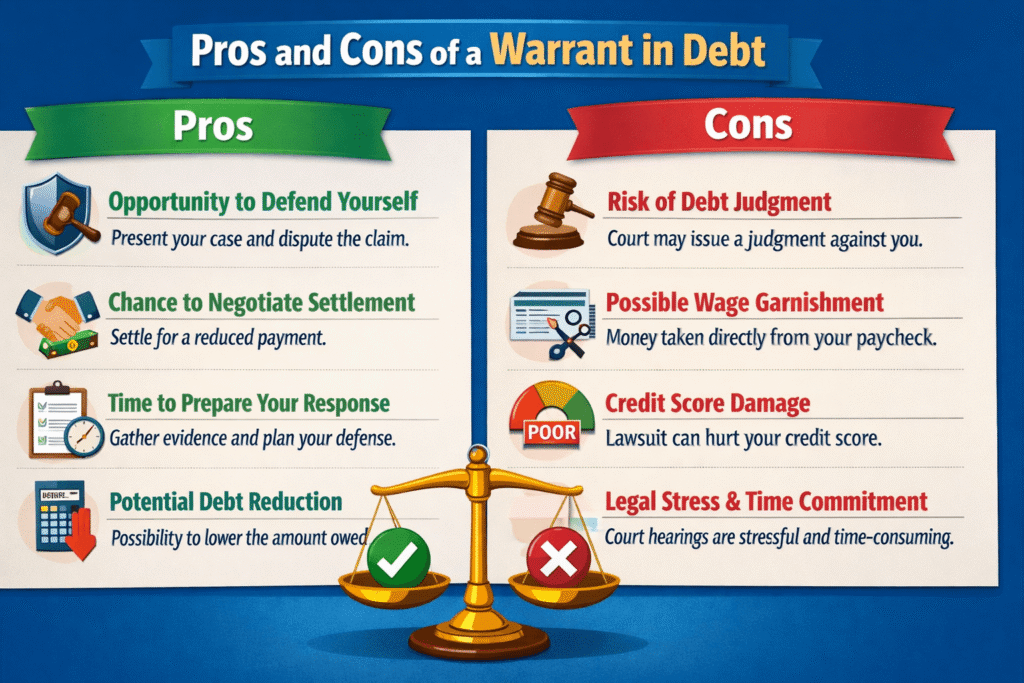

Pros and Cons of a Warrant in Debt

Receiving a warrant in debt may feel overwhelming, but it also gives you an opportunity to take control of your financial situation. Understanding both the advantages and disadvantages can help you respond strategically.

Pros

Opportunity to Defend Yourself A warrant in debt gives you the chance to present your side of the story. If the amount is incorrect or the debt is not yours, you can challenge it in court.

Chance to Negotiate Settlement Many creditors are willing to negotiate before or even during the hearing. This is especially common in a debt collector lawsuit, where collectors often accept reduced payments.

Time to Prepare Your Response Unlike sudden collection actions, a warrant in debt gives you advance notice. You can gather documents, verify the claim, and prepare your defense.

Potential Debt Reduction Sometimes creditors agree to reduce the amount owed, especially when you show willingness to resolve the issue.

Cons

Risk of Debt Judgment If you lose the case, the court may issue a debt judgment against you. This gives the creditor legal power to collect the money.

Possible Wage Garnishment Once a creditor wins a civil lawsuit, they may request wage garnishment, which allows them to take money directly from your paycheck.

Credit Score Damage A debt lawsuit or court ruling can negatively impact your credit score and remain on your credit report for years.

Legal Stress and Time Commitment Attending hearings, responding to documents, and handling a court summons can be stressful and time-consuming.

Is a Warrant in Debt the Same as an Arrest Warrant?

This is the biggest fear people have, so let’s clear it up right now! No, it is absolutely not an arrest warrant!

You cannot go to jail simply for owing a debt. A warrant in debt is strictly a civil case, not a criminal case. The police are not looking for you, and you are not in trouble with the law. It is simply a formal financial dispute between you and a creditor. Take a deep breath and relax!

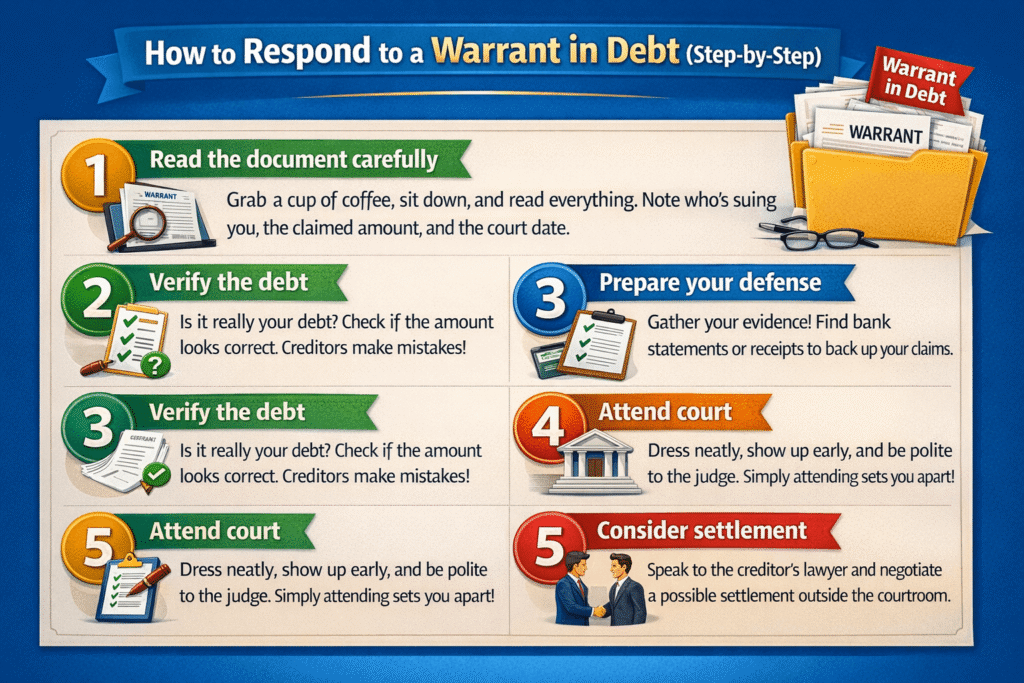

How to Respond to a Warrant in Debt (Step-by-Step)

Acting quickly is your superpower here! Follow these exciting, proactive steps to handle the situation like a pro.

Step 1: Read the document carefully

Grab a cup of coffee, sit down, and read every single word. Look for who is suing you, the exact amount they claim you owe, and the court date.

Step 2: Verify the debt

Is this actually your debt? Ask yourself if the amount looks correct. Creditors make mistakes all the time!

Step 3: Prepare your defense

Gather your evidence! If you already paid the debt, find the bank statements. If the amount is wrong, get your receipts.

Step 4: Attend court

Dress neatly, show up early, and be polite to the judge. Simply showing up puts you ahead of the game, as many people never even go!

Step 5: Consider settlement

You can often talk to the creditor’s lawyer right outside the courtroom. They might agree to lower the total amount or set up a monthly payment plan if you just ask!

What Happens If You Ignore a Warrant in Debt?

Throwing the paper in the trash is the worst thing you can do! If you ignore it, the creditor automatically wins. This is called a “default judgment.”

Once they have a default judgment, they can ask the court to garnish your wages (take money straight out of your paycheck!) or put a levy on your bank account. It also causes massive credit damage. If your wages get slashed, you’ll need to figure out how to save money fast just to cover your basic living expenses. So, whatever you do, do not ignore the notice!

The Federal Trade Commission explains that ignoring a debt lawsuit can lead to default judgments and potential wage garnishment.

Can You Fight a Warrant in Debt?

Yes, you absolutely can! You have rights, and fighting back is entirely possible.

Incorrect amount

If they added hundreds of dollars in illegal fees, you can challenge the total balance.

Identity theft

If someone stole your identity and opened a credit card in your name, you do not owe that money! Bring your police report to court.

Expired debt (statute of limitations)

Did you know debts have an expiration date? If a debt is too old (usually 3 to 6 years, depending on your state), they legally cannot sue you for it anymore!

Lack of proof

Collection agencies buy debts in massive spreadsheets. Often, they do not have the original signed contract to prove you actually owe the money!

How a Warrant in Debt Affects Your Credit Score

You are probably wondering about your warrant in debt credit score impact. A court judgment can stay on your public record and significantly hurt your credit score. It shows future lenders that you did not pay a past obligation, making it harder to rent an apartment or buy a car. The collection accounts associated with the lawsuit will also drag your score down for up to seven years.

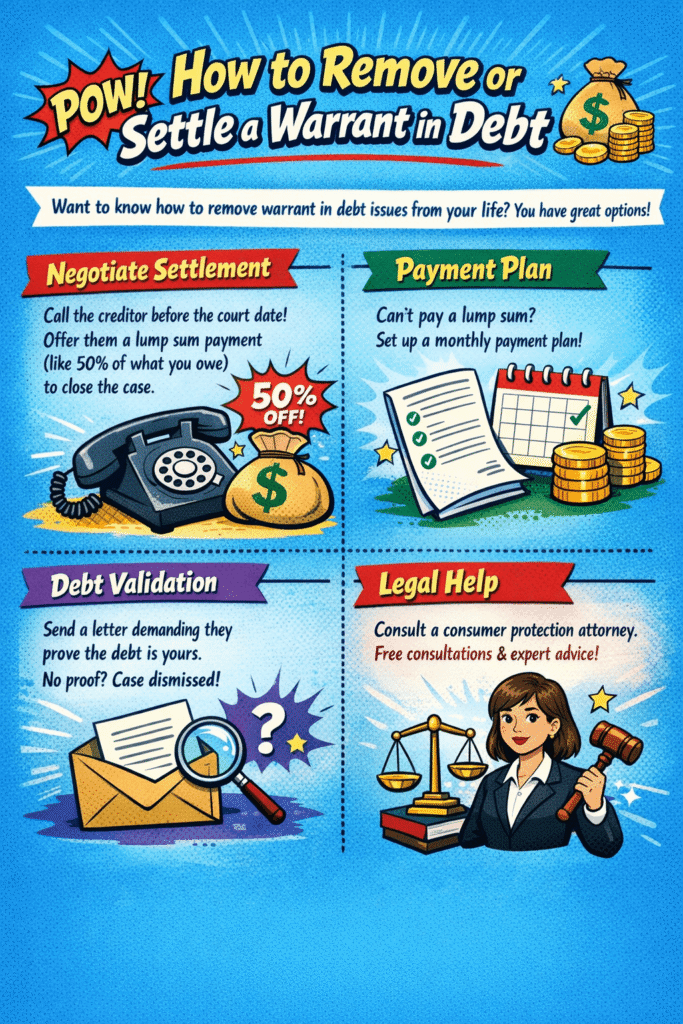

How to Remove or Settle a Warrant in Debt

Want to know how to remove warrant in debt issues from your life? You have great options!

Negotiate settlement

Call the creditor before the court date! Offer them a lump sum payment (like 50% of what you owe) to close the case.

Payment plan

If you cannot pay a lump sum, ask to set up a monthly payment plan. When you know how to manage money effectively, carving out a small monthly payment is totally doable!

Debt validation

Send a formal letter demanding they prove the debt is yours. If they can’t, the court might dismiss the case.

Legal help

Don’t be afraid to consult a consumer protection attorney. Many offer free initial consultations and can give you amazing advice!

Warrant in Debt Example (Real-Life Scenario)

Let’s look at a helpful warrant in debt example to see how this works in the real world!

Meet John. John had a $2,000 credit card bill he couldn’t pay when he lost his job. Two years later, a debt buyer purchased his account and filed a warrant in debt. John panicked at first, but then he took action! He went to court on his scheduled date. Before the judge even called his name, John spoke to the creditor’s lawyer in the hallway. They agreed that John would pay $1,000 in a lump sum, and they dropped the lawsuit. John saved his credit and $1,000!

Warrant in Debt vs Summons (Important Comparison Table)

Legal words can be confusing! Let’s clear up the warrant in debt vs summons debate with this easy-to-read table:

Feature

Warrant in Debt

Summons

Main Purpose

Debt-related case

General legal notice

Case Type

Civil case

Could be civil or criminal

Core Issue

Payment dispute

Various legal issues (divorce, lawsuits, etc.)

Frequently Asked Questions

Is a warrant in debt serious?

Yes! It is a serious legal action that can lead to wage garnishment, but it is highly manageable if you take action immediately.

Can you go to jail for a warrant in debt?

Absolutely not! It is a civil financial matter, not a criminal one.

How long does a warrant in debt last?

If they get a judgment against you, it can last for 10 to 20 years depending on your local laws, and they can keep trying to collect that money!

Can you settle before court?

Yes! In fact, creditors love it when you call them to settle before court because it saves them time and lawyer fees.

Do you need a lawyer?

You can represent yourself (called going pro se), but consulting a lawyer is always a fantastic idea if the debt is very large or complicated.

Final Thoughts

Receiving legal papers is scary, but you now have the knowledge you need to take control! Don’t panic, take action quickly, and know your rights. By responding to the notice and facing the situation head-on, you can protect your finances and get back on track.

Remember, financial bumps in the road happen to the best of us! Setting up strong financial habits, like learning great budgeting tips, will help keep you out of court and confidently moving toward a bright, debt-free future!

Sabir Abdirahman Mohamed is the founder of ThinkFixer and a personal finance and digital growth writer. He helps beginners learn how to save money, build online income streams, and grow blogs or businesses through practical SEO strategies. His content focuses on budgeting, smart money management, realistic ways to make money online, and step-by-step blogging guidance. His mission is to make financial and digital knowledge simple, actionable, and accessible for everyone.

")

")