What Is In House Financing? (Complete Guide for Beginners)

Struggling to get approved for a bank loan? You are not alone. In-house financing gives buyers another way to pay for expensive purchases when traditional lenders say no. Instead of borrowing from a bank or credit union, you borrow directly from the business selling the product or service. This option is common for cars, furniture, medical procedures, and even real estate. In this guide, you will learn what in-house financing means, how it works, its pros and cons, and when it makes sense to use it.

If you are wondering what is in house financing and whether it is the right option for you, understanding the basics can help you make a smarter financial decision.

Table of Contents

What Is In House Financing? In House Financing Meaning (Simple Definition)

In-house financing is a type of loan where a business sells a product and provides the financing directly to the customer, instead of using a bank or third-party lender. The buyer makes payments directly to the seller under agreed terms.

So, what is in house financing in simple terms? It is a financing method where the seller handles both the sale and the loan process.

In simple terms, if you have been asking what does in house financing mean, it means the seller acts as both the store and the lender. This can make approval easier for buyers who have bad credit, no credit history, or need fast financing.

According to Investopedia, in-house financing refers to a situation where a business provides a loan directly to the customer instead of using a third-party lender, making it a more accessible option for buyers with limited credit history.

For example, imagine you are buying a used car. Instead of getting a loan from your bank, the car dealership approves you for a loan directly through their own finance department. If you want to dive deeper into this concept, check out our comprehensive in-house financing guide to learn more.

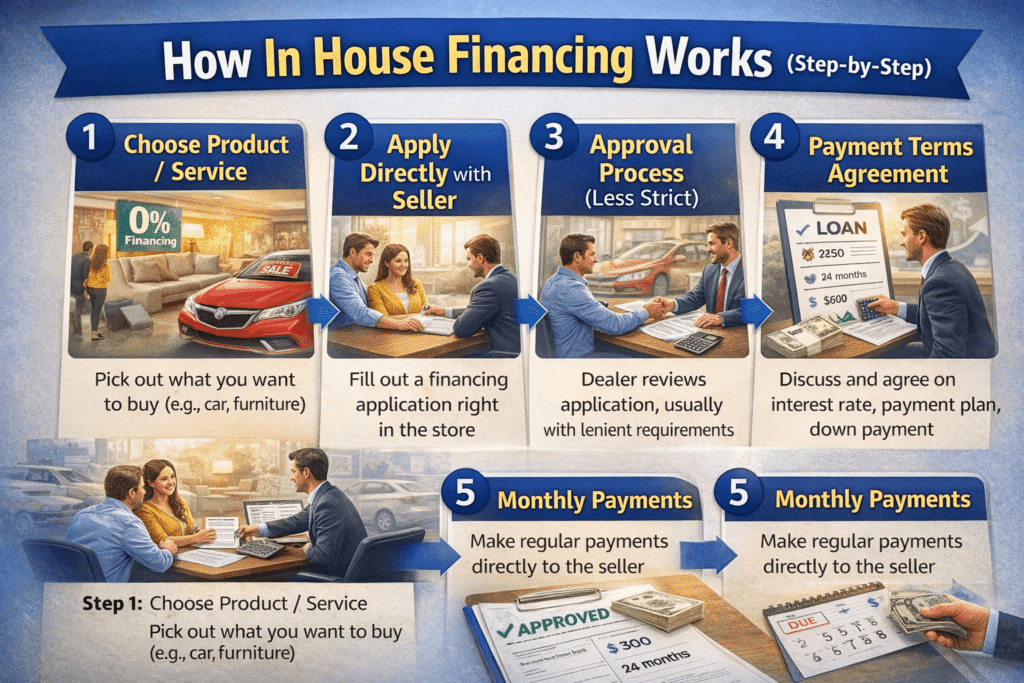

How In House Financing Works (Step-by-Step)

Understanding how in house financing works takes the mystery out of the process. Because the store wants to make a sale, they make the borrowing process as easy as possible. Here is the typical step-by-step journey:

To fully understand what is in house financing, it is important to see how the process works step by step.

Step 1: Choose Product/Service

First, you pick out what you want to buy. This could be a new sofa, a used car, or even dental braces.

Step 2: Apply Directly with Seller

Once you choose your item, you will fill out a financing application right there at the store or clinic. You do not need to visit a bank or fill out separate paperwork elsewhere.

Step 3: Approval Process (Less Strict)

The business will review your application. Because they set their own rules, the approval process is usually much less strict than a traditional bank. They might check your credit score, but they often focus more on your current income and ability to pay.

Step 4: Payment Terms Agreement

If approved, the seller will outline the terms of the loan. This includes your interest rate, your monthly payment amount, the down payment required, and how long you will have to pay off the balance.

Step 5: Monthly Payments

After signing the agreement and paying your down payment, you take the item home. You will then make your scheduled monthly payments directly to the seller until the item is fully paid off.

A classic example is a local furniture store offering “0% down and no credit check” promotions. You pick the living room set, sign the paperwork, and pay the store directly every month.

Why Businesses Offer In House Financing

Businesses offer in-house financing because it helps them close more sales. Many customers want to buy but cannot qualify for traditional loans. By offering direct financing, sellers can approve more buyers, move inventory faster, and earn extra money through interest and fees. For the customer, it creates a more convenient path to ownership. For the business, it creates another source of revenue.

Common Types of In House Financing

In-house financing pops up in several different industries. Here are the most common places you will see it:

Car dealerships (Buy Here Pay Here): These dealerships specialize in selling cars to people with bad credit. Buy here pay here financing means you buy the car on their lot and make payments to them directly.

Furniture stores: Many local and big-box furniture retailers offer payment plans directly to consumers to help them afford large room sets.

Medical/dental financing: Dentists, plastic surgeons, and specialized clinics often offer direct payment plans for expensive procedures not covered by insurance.

Real estate (seller financing): Sometimes, a home seller will act as the bank for the buyer. This is a creative way to purchase property, and if you are looking to manage costs effectively in real estate, it pairs well with knowing how to save building costs.

Retail stores (installment plans): Appliance and electronics stores often let you break up a large purchase into smaller weekly or monthly payments.

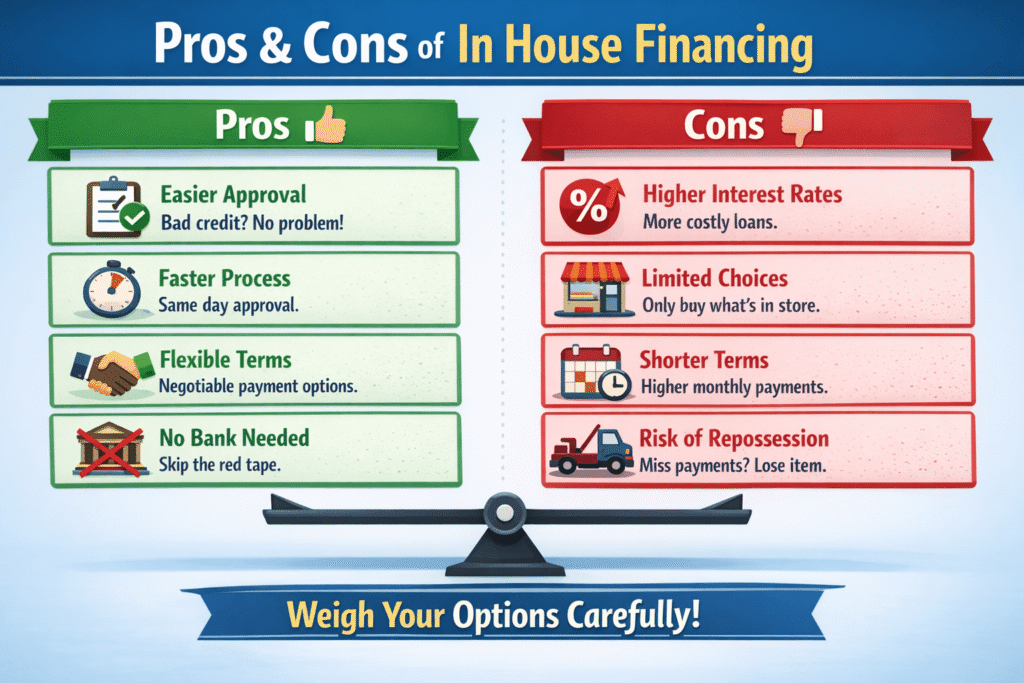

Pros and Cons of In House Financing

Like any financial decision, there are clear benefits and drawbacks to consider. Reviewing the in house financing pros and cons will help you make a smart choice.

Before deciding, it is important to understand what is in house financing and how its advantages and disadvantages can affect your finances.

Pros

Easier approval: Sellers are usually willing to accept buyers with bad credit or no credit history.

Faster process: You can often apply, get approved, and take the item home all in the same day.

Flexible terms: Because you are dealing directly with the seller, you might have room to negotiate the down payment or monthly schedule.

No bank needed: You avoid the red tape, long wait times, and strict requirements of traditional lenders.

Cons

Higher interest rates: To make up for the higher risk of lending to people with lower credit scores, sellers usually charge more in interest.

Limited choices: You can only buy what that specific store sells.

Shorter repayment terms: You often have less time to pay off the loan compared to a bank, which can make monthly payments higher.

Risk of repossession: If you miss payments, the seller can act quickly to take the item back.

In House Financing vs Traditional Financing

How does borrowing directly from a seller compare to walking into a bank? Knowing the difference can help you navigate broader finance trends and choose the right path for your wallet.

Many buyers compare in-house financing with traditional loans before making a decision. The biggest difference is that with in-house financing, the seller provides the loan directly, while a bank loan comes from a separate financial institution. Here is how they compare:

Feature

In House Financing

Traditional Bank Loan

Approval

Easy (Lenient requirements)

Strict (Rigid requirements)

Credit Check

Low / None

High (Focuses heavily on score)

Interest Rate

Higher

Lower

Speed

Fast (Often same-day)

Slower (Can take days or weeks)

In general, traditional financing is cheaper if you qualify, while in-house financing is easier to access if your credit history is weak.

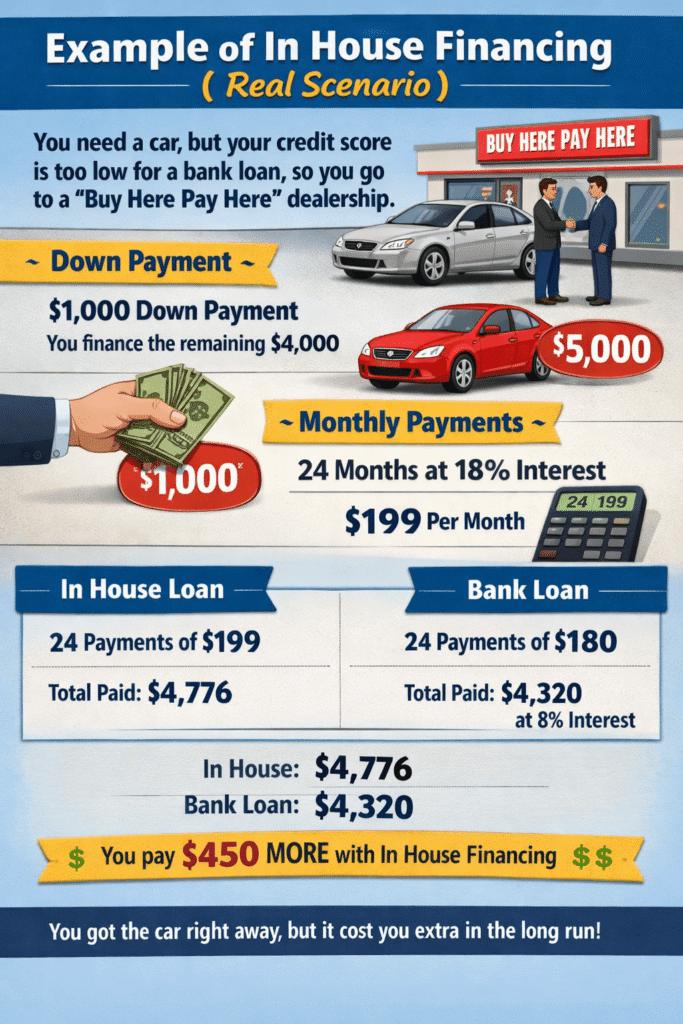

Example of In House Financing (Real Scenario)

Let’s look at a realistic example of how this works. Imagine you need a reliable vehicle for work, but your credit score is too low for a bank loan. You visit a local “buy here pay here” dealership and find a car priced at $5,000.

Down payment: The dealer asks for $1,000 down. You now need to finance the remaining $4,000.

Monthly payment breakdown: The dealer offers you a 24-month payment plan at an 18% interest rate. Your monthly payment comes out to roughly $199.

Total cost vs bank loan: Over 24 months, you will pay about $4,776 for that $4,000 loan. If you had gone to a bank and qualified for an 8% interest rate, your payment would be around $180, and you would only pay $4,320 in total.

This scenario shows that while the in-house option got you the car you needed immediately, it cost you about $450 more in interest over two years.

Interest Rates and Costs Explained

The biggest downside of in-house financing is usually the total cost. Since the seller is lending to buyers who may have lower credit scores or limited borrowing history, they often charge higher interest rates to reduce their risk.

That means the monthly payment may look manageable, but the total amount paid over time can be much higher than expected. Some sellers may also add late fees, processing charges, service fees, or early payoff penalties. Before agreeing to any loan, review the annual percentage rate, the full repayment amount, and every fee listed in the contract.

The Consumer Financial Protection Bureau advises consumers to carefully review loan terms, interest rates, and fees before agreeing to any financing arrangement, especially when dealing with non-traditional lenders.

How to Qualify for In House Financing

Qualifying for in-house financing is usually easier than qualifying for a traditional bank loan, but businesses still want to see that you can repay what you borrow. In many cases, sellers may ask for proof of income, a government-issued ID, proof of address, a down payment, and personal references. Some may check your credit score, while others focus more on your employment status and monthly income. Because approval rules vary by seller, it is always smart to ask what documents you need before you apply.

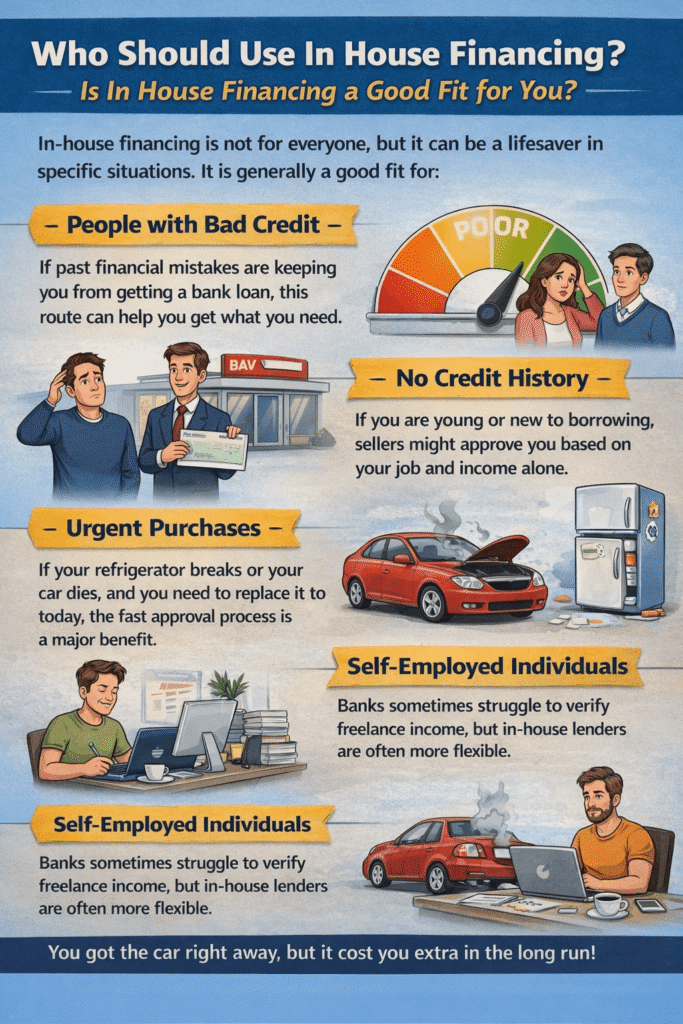

Who Should Use In House Financing?

Knowing what is in house financing can help you decide if this option fits your current financial situation.

In-house financing is not for everyone, but it can be a lifesaver in specific situations. It is generally a good fit for:

People with bad credit: If past financial mistakes are keeping you from getting a bank loan, this route can help you get what you need.

No credit history: If you are young or new to borrowing, sellers might approve you based on your job and income alone.

Urgent purchases: If your refrigerator breaks or your car dies, and you need to replace it today, the fast approval process is a major benefit.

Self-employed individuals: Banks sometimes struggle to verify freelance income, but in-house lenders are often more flexible.

If you are currently in a tight spot and need to build up your down payment quickly, learning how to save money fast can make your financing terms much more affordable.

Who Should Avoid It?

While helpful for some, certain people should steer clear of borrowing directly from a seller:

People with good credit: If your credit score is high, you will almost always get a much better interest rate from a traditional bank or credit union.

Long-term financing needs: If you are buying something you need to pay off over 5 to 10 years, the high interest rates of in-house loans will cost you a fortune.

Those sensitive to high interest: If your budget is incredibly tight, adding high-interest debt could push you into deeper financial trouble.

Risks of In House Financing

Borrowing through in-house financing comes with real risks, especially if you rush into an agreement without reading the full contract.

The first risk is overpaying. A loan with a higher interest rate can make the final cost much greater than the original price of the item. The second risk is fast repossession. In vehicle financing, some sellers can act quickly when payments are missed. Another risk is unclear contract language. Some agreements include extra fees, strict default terms, or confusing conditions that many buyers overlook.

The safest approach is to review every detail before signing and make sure you understand exactly what happens if you miss a payment.

Tips Before Choosing In House Financing

Before you sign on the dotted line, take a step back and protect yourself with these simple tips:

Compare total cost, not monthly payment: Multiply the monthly payment by the number of months in the loan, then add your down payment. Is the item really worth that final number?

Read the contract carefully: Look for hidden fees, late payment penalties, and the exact interest rate.

Negotiate terms: Unlike banks, sellers want to move inventory. Try to negotiate a lower price on the item or a lower interest rate.

Check seller reputation: Look up online reviews. Do they have a history of treating buyers unfairly?

Making smart borrowing decisions all comes down to having the right money mindset. Taking a few extra minutes to review the deal can save you hundreds, if not thousands, of dollars.

Frequently Asked Questions (FAQ Section)

What is in house financing and how does it work?

What is in house financing? It is a type of loan where the seller provides financing directly to the buyer instead of using a bank. The buyer then repays the seller in monthly installments based on agreed terms.

Is in house financing a good idea?

In-house financing can be a good idea for buyers with bad credit, no credit history, or urgent purchasing needs. However, it is usually more expensive than traditional financing, so comparing offers first is important.

Does it affect your credit score?

It can affect your credit score if the lender reports your payments to the credit bureaus. Some in-house lenders report on-time payments, while others only report missed payments or defaults.

Can you refinance later?

Yes, many buyers refinance later with a bank or credit union after improving their credit score. This can lower the interest rate and reduce the total cost of the loan.

Is it the same as dealer financing?

Not always. Dealer financing may involve a dealership arranging a loan through a third-party lender, while in-house financing means the seller provides the loan directly.

Do you need a down payment?

In many cases, yes. Most in-house lenders require a down payment to reduce their risk and lower the amount being financed.

Final Verdict (Conclusion)

Now that you understand what is in house financing, you can better evaluate whether it is the right option for your needs.

In-house financing can make it possible to buy a car, furniture, medical treatment, or other important items when traditional lenders are not an option. It offers easier approval, faster processing, and more flexibility for buyers with bad credit or limited credit history.

However, those benefits often come with higher interest rates, extra fees, and stricter repayment risks. That is why the best approach is to compare the total cost, read the contract carefully, and explore bank or credit union loans before making a final decision.

If you need fast approval and have few alternatives, in-house financing may be the right short-term solution. But if you qualify for lower-cost financing elsewhere, that will usually save you more money in the long run.

Sabir Abdirahman Mohamed is the founder of ThinkFixer and a personal finance and digital growth writer. He helps beginners learn how to save money, build online income streams, and grow blogs or businesses through practical SEO strategies. His content focuses on budgeting, smart money management, realistic ways to make money online, and step-by-step blogging guidance. His mission is to make financial and digital knowledge simple, actionable, and accessible for everyone.

")

")

")