Foreclosure Bailout Loan: How to Save Your Home Before It’s Too Late

Falling behind on mortgage payments can quickly lead to serious financial consequences, including foreclosure. If you have received a foreclosure notice, it’s important to understand that you may still have options to protect your home and regain financial stability.

A foreclosure bailout loan is one option homeowners use to catch up on missed payments and stop the foreclosure process. Even if things look completely overwhelming right now, you have powerful tools available to protect your most valuable asset.

In this guide, you’ll learn how foreclosure bailout loans work, who qualifies, potential risks, and alternative options. the exact steps to get one, and how to stop the bank from taking your home. We will walk through the absolute best options out there, share some super helpful tips, and show you exactly how to rebuild your financial confidence! Let’s dive right in and save your home!

Foreclosure bailout loans are often used by homeowners who have temporary financial difficulties but still have equity in their homes. These loans are typically short-term and may carry higher interest rates, so it’s important to carefully review all terms before proceeding.

Table of Contents

What Is a Foreclosure Bailout Loan?

Let’s start with the basics! A foreclosure bailout loan is a short-term, specialized loan designed to help homeowners catch up on missed mortgage payments and stop foreclosure dead in its tracks. These loans are typically used as short-term financial solutions for homeowners facing imminent foreclosure.

When you miss a few mortgage payments, your lender will eventually issue a notice of default. At this stage, a foreclosure bailout loan may help cover missed payments and stop the foreclosure process. You borrow against the equity you have built up in your home, use that fresh cash to pay off your past-due balance, and officially stop the foreclosure process.

Who offers it? You won’t usually find these loans at massive traditional banks. Instead, they are typically offered by private lenders, hard money lenders, and specialized mortgage rescue companies that understand you need help right now, not three months from now!

Example: Let’s say you owe $15,000 in past-due mortgage payments. A lender approves you for a foreclosure rescue loan based on the equity in your house. The lender pays the $15,000 directly to your mortgage company. Once the past-due balance is paid, the foreclosure process is typically paused or stopped. and you simply repay the new lender over an agreed period.

According to the U.S. Department of Housing and Urban Development, homeowners facing foreclosure may qualify for assistance programs designed to help them avoid losing their homes.

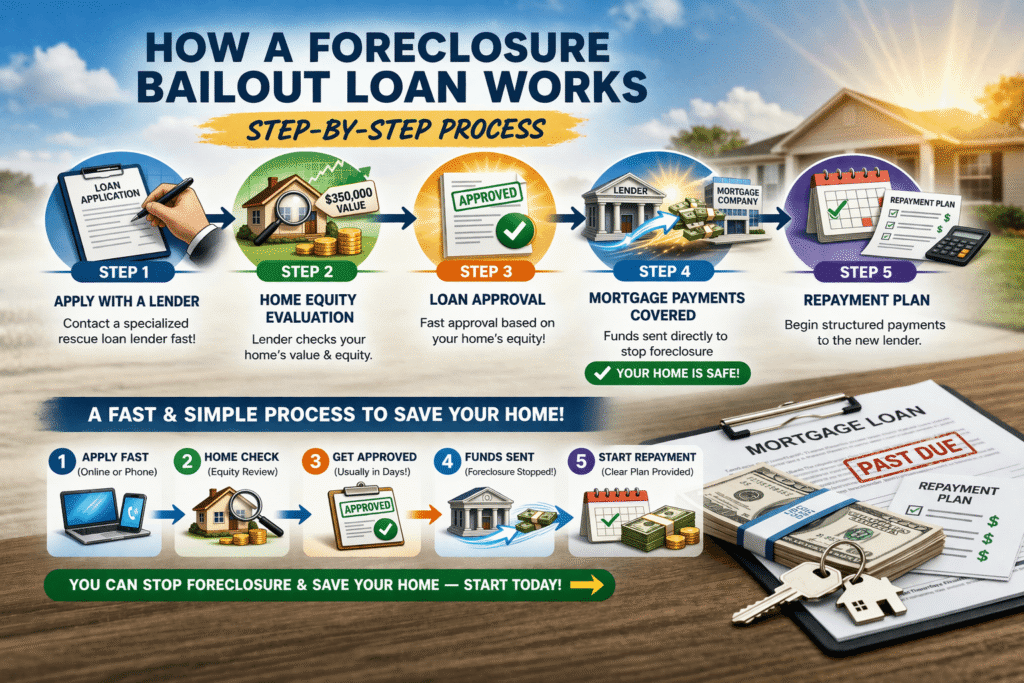

How a Foreclosure Bailout Loan Works (Step-by-Step)

Getting an emergency mortgage loan might sound complicated, but I promise you it is actually a straightforward process! Here is exactly how it works, step-by-step:

Step 1: Apply with a Lender

First things first! You need to reach out to a specialized lender who deals with rescue loans. Because time is ticking, you want to apply as soon as you realize you need a loan to stop foreclosure.

Step 2: Home Equity Evaluation

The lender needs to know how much your home is worth. They will look at the current market value of your property and subtract what you still owe. The difference is your equity. The more equity you have, the easier this process will be!

Step 3: Loan Approval

Once the lender confirms your home has enough equity to cover the risk, they will approve your loan. Since these lenders care more about your home’s value than a perfect financial history, approval happens much faster than a standard bank loan!

Step 4: Mortgage Payments Covered

Once approved, the lender releases funds to cover missed mortgage payments. The lender releases the funds. Usually, they send the money straight to your primary mortgage lender to instantly cure the default. Just like that, your home is safe!

Step 5: Repayment Plan

Now that the immediate crisis is over, you begin making payments to your new lender. You will get a clear, structured repayment plan so you know exactly what to pay and when.

Who Qualifies for a Foreclosure Bailout Loan?

You might be thinking, “This sounds amazing, but will I even qualify?” Eligibility requirements vary by lender, but common criteria include:

Because these loans are designed for emergencies, the rules are totally different. Here is what you generally need:

Home Equity Required: This is the big one! Lenders typically want to see that you have at least 30% to 40% equity in your home. Your house is acting as the security for the loan.

Proof of Income: You need to show the lender that you have money coming in to afford the new loan payments. Pay stubs, tax returns, or bank statements showing steady deposits are perfect.

Foreclosure Notice: Lenders will ask to see your notice of default to verify exactly how much you need to catch up.

Credit Score (Low Credit Accepted): Good news! You absolutely do not need a perfect credit score! Since the loan relies heavily on home equity, lenders are highly forgiving of bad credit. If you are exploring bad credit options, you already know that poor credit isn’t the end of the road. In fact, even if you are looking at no credit financing, you might still qualify as long as your home holds enough value!

7 Best Foreclosure Bailout Loan Options

Ready to look at your specific choices? Common foreclosure bailout loan options include:

1. Hard Money Loans

Hard money loans are incredible for speed! Private investors or specialized companies offer these loans based almost entirely on your home’s value, rather than your credit score. They have higher interest rates, but they can fund in a matter of days.

2. Home Equity Loans

If your credit hasn’t taken a massive hit yet, a traditional home equity loan is a wonderful option! You borrow a lump sum against the value of your house at a fixed interest rate. It’s a highly predictable way to get back on track.

3. Cash-Out Refinance

With a cash-out refinance, you completely replace your old mortgage with a brand new one that is larger than what you currently owe. You take the extra “cash out” and use it to catch up on everything else!

4. Private Lenders

Private lenders are individuals or small investment groups who lend out their own capital. Because they aren’t bound by big bank rules, they can offer incredibly flexible, creative solutions!

5. Government Assistance Programs

Always check to see what federal or state programs are available to you! Some states offer massive grants or zero-interest loans specifically designed to act as a save home from foreclosure loan.

6. Reverse Mortgage (For Seniors)

If you are 62 or older, a reverse mortgage is a phenomenal tool! You can convert part of your home equity into cash without having to make a monthly mortgage payment, instantly solving the foreclosure threat.

7. Bridge Loans

A bridge loan is a super short-term loan meant to “bridge the gap.” If you plan to sell your home eventually but need to stop the foreclosure right now, a bridge loan buys you the precious time you need! Similar to in-house financing, bridge loans are a helpful alternative lending model when you need custom solutions.

Pros and Cons of Foreclosure Bailout Loans

Like any financial solution, foreclosure bailout loans have advantages and risks. and a few things to watch out for! Let’s look at both sides so you can make an incredibly informed decision.

Pros

Stop foreclosure quickly: The number one benefit! These loans move at lightning speed to halt the legal process.

Keep your home: You don’t have to pack up your life. You get to stay right where you belong.

Flexible approval: No perfect credit? No problem! The equity in your house does the heavy lifting for you.

Cons

High interest rates: Because the lender is taking on more risk, they will charge a higher interest rate than a standard bank.

Short repayment period: You usually need to pay these loans back faster, sometimes in just a few years.

Risk of losing home again: If you default on this new loan, you could face foreclosure again. You must make sure the new payments fit perfectly into your monthly budget!

How to Get a Foreclosure Bailout Loan Fast

Because foreclosure timelines can be short, acting quickly is important. If you need to act right now, follow these exact steps:

Check Home Equity: Jump online and look at estimates for your home’s value on sites like Zillow or Redfin. Subtract your current mortgage balance. Is the number positive? That’s your equity!

Compare Lenders: Do not just take the first offer! Call three different private lenders or mortgage brokers and compare their rates.

Prepare Documents: Gather your recent mortgage statements, income proof, and the dreaded foreclosure notice. Having these in a neat folder will speed up everything!

Apply Immediately: Do not wait until the last minute! The closer you get to a foreclosure auction date, the harder it is to stop. Apply today!

Foreclosure Bailout Loan Requirements

To make the application process incredibly smooth and delightfully fast, you want to be prepared. Common documents required include:

Mortgage Statement: Your most recent bill showing exactly what you owe.

Foreclosure Notice: The official document from the lender showing the default amount and any upcoming deadlines.

Income Proof: Two recent pay stubs, your last two years of W2s, or bank statements showing consistent cash flow.

Home Value Estimate: An appraisal or a recent property tax assessment to prove your home’s worth.

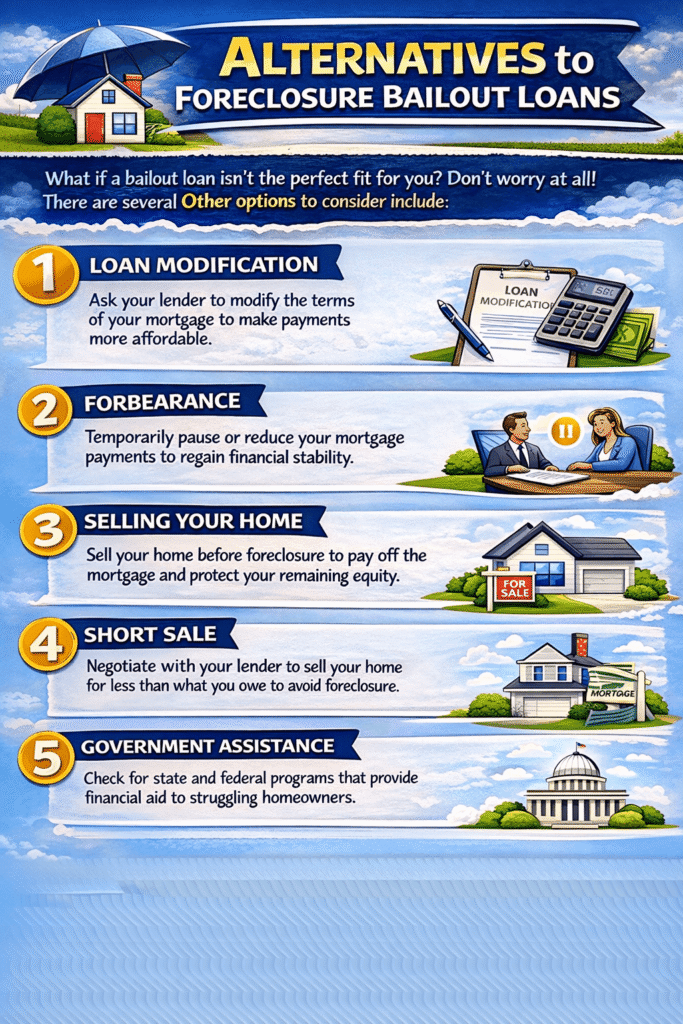

Alternatives to Foreclosure Bailout Loans

What if a bailout loan isn’t the perfect fit for you? Do not worry at all! There are several Other options to consider include:

Loan Modification

You can ask your current lender to change the terms of your loan! They might lower your interest rate, extend the life of the loan, or add your missed payments to the back of the loan.

Forbearance

A forbearance agreement allows you to pause or lower your mortgage payments for a set period while you get back on your feet. It’s like hitting the pause button on your financial stress!

Selling Your Home

If the monthly payments are simply too high, selling your home before the bank takes it is an incredibly smart move! You pay off the mortgage, keep the remaining equity, and start fresh somewhere new.

Short Sale

If you owe more than the house is worth, your lender might agree to a short sale. This means they let you sell the home for less than the mortgage balance and forgive the rest of the debt.

Government Assistance

Look into the Homeowner Assistance Fund (HAF) in your state. This is essentially free money designed to help homeowners catch up on housing-related costs! Exploring these options is just like seeking out alternative financing—there is always more than one way to solve a problem!

The Consumer Financial Protection Bureau recommends exploring loan modification, forbearance, or repayment plans before proceeding with new borrowing options.

Homeowners may also benefit from assistance programs offered through Fannie Mae, which provides options to help borrowers stay in their homes.

Best Lenders Offering Foreclosure Bailout Loans

Finding the right partner to help you through this is crucial! While traditional banks might turn you away, These Common lender types include:

Private Lenders: Individuals who invest their own money in real estate. They are incredibly flexible and easy to talk to!

Hard Money Lenders: Specialized companies that lend strictly based on your property’s value. They are lightning-fast!

Local Credit Unions: If you have been a member for a long time, local credit unions often have special hardship programs and are much more compassionate than big national banks.

Mortgage Rescue Companies: Firms specifically built to help homeowners navigate defaults. They offer custom-tailored emergency loans!

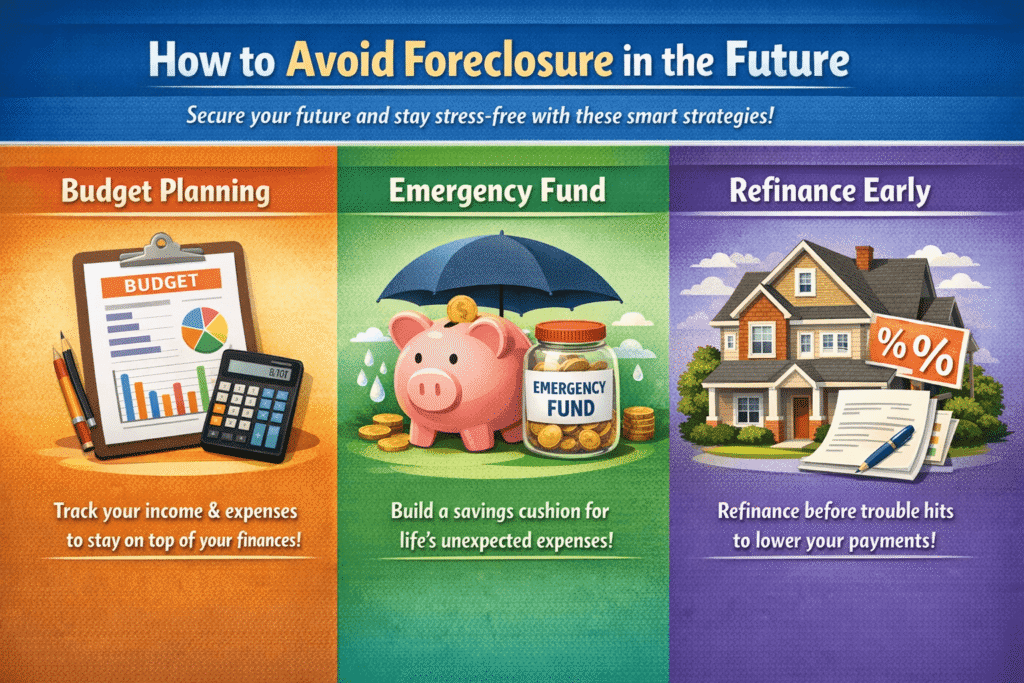

How to Avoid Foreclosure in the Future

Once you have secured your foreclosure rescue loan and stopped the bank in its tracks, it is time to look forward! Let’s make sure you never have to feel this stress ever again.

Budget Planning: It is time to track every single dollar! Understanding your income vs expenses is the absolute best way to ensure your mortgage is always the first thing paid every month.

Emergency Fund: Life happens! Cars break down, roofs leak, and jobs change. Aim to build a small safety net. If you need a quick boost, learn how to save money fast so you always have a cushion to fall back on.

Refinance Early: If you notice your budget getting uncomfortably tight, don’t wait for a missed payment! Refinance your home while your credit is still excellent to lock in a lower, more comfortable monthly payment.

Frequently Asked Questions (FAQ)

Can I get a foreclosure bailout loan with bad credit? Yes, absolutely! Because the loan is secured by the equity in your home, lenders are highly willing to overlook a low credit score.

How fast can I get approved? Incredibly fast! Hard money lenders and private investors can often approve your application in just 24 to 48 hours, and fund the loan within a week or two.

Are foreclosure bailout loans safe? Yes, they are a legitimate tool to save your home! However, you must read the terms carefully. Make sure you understand the interest rate and ensure that you can comfortably afford the new monthly payment.

What happens if I can’t repay? This is important to know! If you default on your new emergency loan, the new lender has the right to foreclose on your home. That is why creating a rock-solid monthly budget is so important once your crisis is solved!

Final Thoughts: Is a Foreclosure Bailout Loan Worth It?

Facing foreclosure can be overwhelming, but several financial solutions may help protect your home. But as you have learned, a foreclosure bailout loan is an incredibly powerful tool that can stop the legal process, catch you up on your missed payments, and most importantly, let you keep the home you love!

If you have equity in your house and a steady income, an emergency mortgage loan is absolutely worth it to save your property. It provides immediate relief and gives you the breathing room you need to get your financial life back on track!

Don’t let fear paralyze you! If you are holding onto a foreclosure notice right now, take a deep breath, review your home’s equity, and start reaching out to lenders today. You have the power to fix this, and you can absolutely do it!

Sabir Abdirahman Mohamed is the founder of ThinkFixer and a personal finance and digital growth writer. He helps beginners learn how to save money, build online income streams, and grow blogs or businesses through practical SEO strategies. His content focuses on budgeting, smart money management, realistic ways to make money online, and step-by-step blogging guidance. His mission is to make financial and digital knowledge simple, actionable, and accessible for everyone.

")

")