Are you struggling to keep up with your monthly mortgage payments? You are not alone. When housing costs feel overwhelming, keeping a roof over your head without draining your bank account becomes the top priority. If you need to reduce mortgage payments quickly, you have likely come across two main options: modifying your current loan or getting a brand-new one.

Understanding the difference between a refinance mortgage vs modification is the first step to reclaiming your financial peace of mind. Both options can lower your monthly bills, but they are designed for very different situations.

In this guide, we will break down exactly how each path works. We will compare costs, credit requirements, and long-term impacts to help you make the smartest choice for your home and your budget in 2026.

Loan Modification vs Refinance (Quick Comparison Table)

If you want a fast breakdown, here is how the two options stack up against each other.

Factor

Loan Modification

Refinance

Definition

Changes the terms of your current mortgage to make payments affordable.

Replaces your current mortgage with a brand-new loan.

Requires New Loan

No.

Yes.

Credit Score Needed

Low or none (based on financial hardship).

Good to excellent (usually 620+).

Best For

Borrowers facing financial hardship who cannot afford current payments.

Borrowers with good credit looking to lock in lower interest rates.

Costs

Usually free or involves minimal administrative fees.

High (closing costs range from 2% to 5% of the loan amount).

Table of Contents

What Is Loan Modification?

A loan modification is exactly what it sounds like. Instead of getting a new loan, your lender agrees to modify the rules of your existing mortgage. Think of it like renegotiating a contract. The goal of this home loan restructuring is to make your monthly payments affordable so you can keep your home and avoid foreclosure.

When you apply for a modification, you ask your lender for help. You must prove that you are going through a financial hardship, such as a job loss, medical emergency, or divorce. If the lender approves, they will adjust the math on your mortgage to bring your monthly bill down to a level you can actually pay.

Types of Loan Modifications

Lenders use a few different tools to lower your payment. They might use one or a combination of the following:

Rate reduction: The lender lowers your interest rate. Even a slight drop can save you hundreds of dollars a month.

Term extension: The lender stretches your loan out over a longer period. For example, they might turn a 30-year loan into a 40-year loan. You pay more interest over time, but your monthly bill shrinks.

Principal forbearance: The lender sets aside a portion of your loan balance. You do not pay interest on this set-aside amount, which lowers your payment. You will eventually have to pay it back, usually when you sell the house or finish paying off the rest of the mortgage.

Who Qualifies for Loan Modification

To qualify, you generally need to prove that you are in financial distress. Lenders want to see that you are either already behind on your payments or that you are about to fall behind. You will need to provide bank statements, pay stubs, and a “hardship letter” explaining why you cannot afford your current bill.

What Is Mortgage Refinancing?

Mortgage refinancing is the process of trading in your old mortgage for a new one. The new loan pays off the old loan completely. People usually do this to get a lower interest rate, change their loan term, or tap into their home’s equity.

How Refinancing Works

Refinancing is just like buying your home all over again, minus the moving boxes. You apply for a new loan with a lender (either your current one or a new one). They check your credit, verify your income, and appraise your home’s value. If approved, the new loan takes effect.

Types of Refinancing

There are two main types of refinancing that borrowers use:

Rate-and-term refinance: You change your interest rate, your loan timeline, or both. For example, you might swap a 30-year loan at 7% for a new 30-year loan at 5%.

Cash-out refinance: You take out a new loan that is larger than what you currently owe. You get the difference in cash, which you can use for home repairs or paying off high-interest debt.

Refinance Requirements

Unlike a modification, lenders treat a refinance like a standard loan application. You need a solid credit score (usually at least 620). You also need a stable income, a low debt-to-income ratio, and enough equity in your home. Lenders want proof that you are a safe bet.

Key Differences Between Loan Modification vs Refinance

While the comparison table gives a great overview, let’s dive deeper into what really sets these two mortgage relief options apart.

Credit Score Requirements

Refinancing requires good credit. If your score has dropped because of missed payments, you likely will not qualify. Loan modification, however, is built for people who are struggling. Your current credit score matters much less than your actual ability to pay the new, modified amount.

Costs and Fees

Refinancing is expensive. You have to pay closing costs, which include appraisal fees, title searches, and loan origination fees. This can cost thousands of dollars out of pocket. Loan modifications are typically free. Lenders offer them to prevent the massive costs associated with foreclosing on a home.

Approval Process

The refinance process is strict. It relies heavily on numbers, credit reports, and strict lending guidelines. The modification process is more subjective. It involves proving your hardship and working directly with your lender’s loss mitigation department.

Impact on Credit

A successful refinance usually has a minor, temporary impact on your credit score, similar to applying for any new credit card. A loan modification can hurt your credit score initially, especially if you had to miss payments to qualify or if the lender reports the loan as “paid for less than agreed.”

Long-Term Financial Impact

Refinancing at a lower rate can save you tens of thousands of dollars in interest over the life of the loan. Loan modification often increases the total amount you pay in the long run. By stretching out the loan term or adding missed payments to the back of the loan, you pay more interest overall, even if your monthly bill is lower today.

Loan Modification vs Refinance — Which Is Better for You?

Choosing the right path comes down to your unique situation. Let’s look at a few common scenarios to help you figure out how to best save money and protect your home.

If you are behind on payments: Loan modification is your best bet. A refinance lender will not approve you if you have recent missed mortgage payments.

If you have good credit and stable income: Refinancing is the way to go. You can secure a lower interest rate without the negative credit marks associated with modifications.

If you want long-term savings: Refinancing wins. Lowering your interest rate without stretching out your loan term means you pay less over decades.

If you are in financial hardship: Go with a loan modification. If you lost your job or faced a massive medical bill, a modification provides the immediate safety net you need.

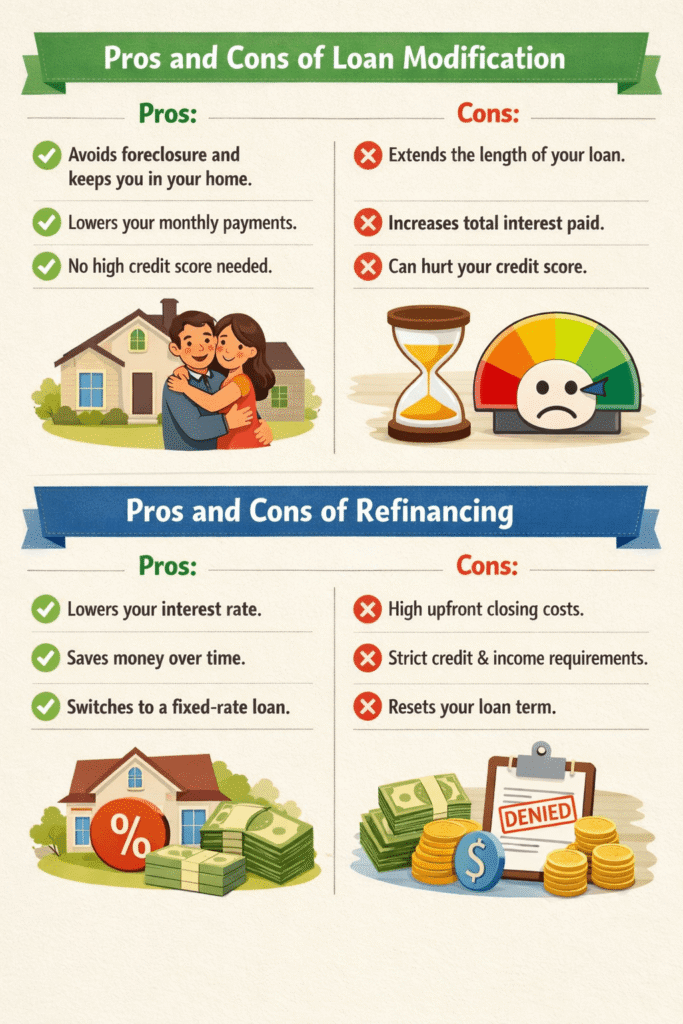

Pros and Cons of Loan Modification

Pros:

Helps you avoid foreclosure and stay in your home.

Provides immediate relief by lowering your monthly payment.

Does not require a high credit score or hefty closing costs.

Cons:

Usually extends the length of your loan.

You will likely pay more total interest over time.

Can negatively impact your credit score.

Pros and Cons of Refinancing

Pros:

Secures a lower interest rate based on market conditions.

Saves you significant money over the lifespan of the loan.

Can allow you to switch from an adjustable rate to a safe, fixed rate.

Cons:

Requires paying thousands of dollars in upfront closing costs.

Strict approval requirements regarding income and credit.

Can reset the clock on your mortgage, keeping you in debt longer if you are not careful.

Real Example: Loan Modification vs Refinance

To see how this works in the real world, let’s look at a practical example.

Imagine you have a $2,000 monthly mortgage payment. You still owe $250,000 on your home, and your interest rate is 6.5%. You recently took a pay cut and can no longer afford the $2,000 bill.

The Loan Modification Route: You contact your lender and prove your hardship. They agree to extend your remaining loan term from 20 years back out to 30 years and drop your rate slightly. Your new payment becomes $1,400 per month. You get immediate relief and keep your house, though you will be paying on it for 10 extra years.

The Refinance Route: Instead of a modification, you decide to refinance because your credit is still excellent. You shop around and find a new lender offering a 5% interest rate on a 20-year loan. You pay $5,000 in closing costs upfront. Your new payment becomes $1,300 per month. You save money every month, and you still pay off the house in 20 years.

Which Option Saves More Money in the Long Run?

If your main goal is to lower housing costs over the entire lifespan of your homeownership, refinancing almost always wins.

When you refinance to a lower interest rate, you reduce the actual cost of borrowing money. Over 15 or 30 years, saving 1% or 2% on interest adds up to massive savings.

Loan modifications, on the other hand, prioritize short-term survival. By stretching your loan out to 40 years, your monthly bill shrinks, but you are paying interest for an extra decade. A modification fixes today’s budget problem, but it costs more by the time you own the home free and clear.

When You Should Avoid Both Options

There are specific times when you need to carefully manage finances and avoid both of these paths.

You should avoid refinancing if you plan to move in the next few years. It takes time to break even on those high closing costs. If you pay $6,000 to close a refinance and save $100 a month, it takes 60 months (5 years) just to break even.

You should avoid a loan modification if your financial hardship is completely permanent and you simply can never afford the house, even with a lower payment. If your income has vanished completely, delaying the inevitable might drain your remaining savings.

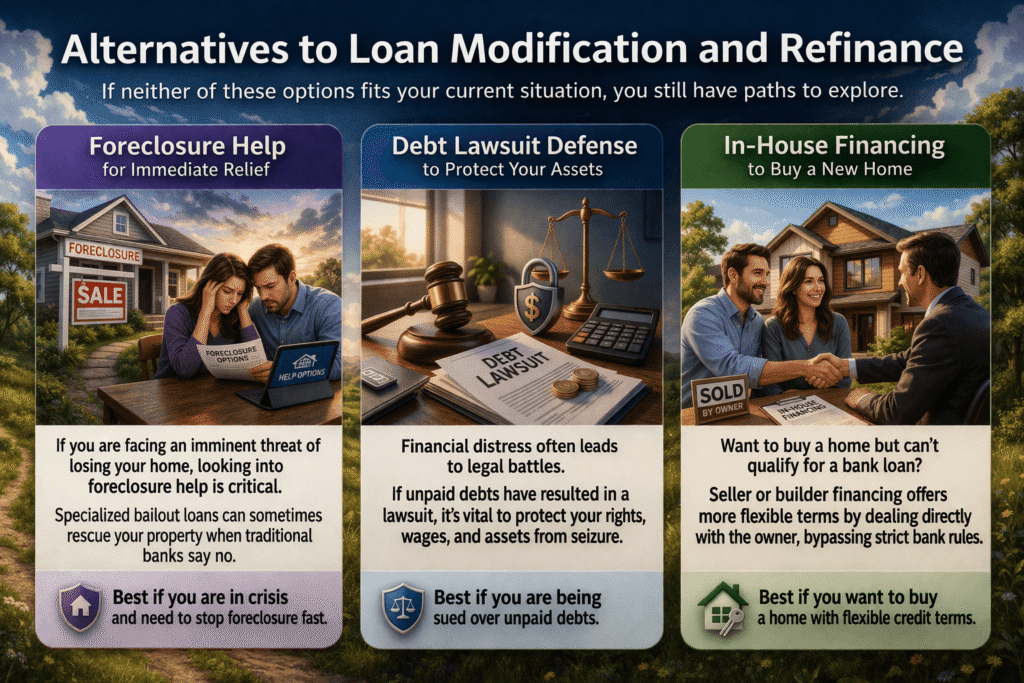

Alternatives to Loan Modification and Refinance

If neither of these options fits your current situation, you still have paths to explore.

If you are facing an imminent threat of losing your home, looking into foreclosure help is critical. Specialized bailout loans can sometimes rescue your property when traditional banks say no.

Financial distress rarely happens in a vacuum. If unpaid debts are leading to aggressive legal actions, understanding how to handle a debt lawsuit is vital to protecting your wages and assets from being seized.

If you are looking to buy a different home entirely but cannot qualify for traditional mortgages, exploring in-house financing could be a great alternative. By dealing directly with a seller or builder, you bypass the strict rules of big banks. Understanding financing pros and cons in these alternative setups can help you stay a homeowner without the traditional red tape.

Loan Modification vs Refinance: Which Is Better?

If you’re struggling financially, loan modification is usually the better option because it helps you stay in your home quickly.

However, if your credit score is strong and you want long-term savings, refinancing is often the better choice.

In most cases:

Choose loan modification if you’re behind on payments

Choose refinance if you want lower interest rates

Choose loan modification if your credit is low

Choose refinance if you want long-term savings

Can You Do Both Loan Modification and Refinance?

Yes, many homeowners first apply for loan modification during financial hardship. After improving their credit and financial situation, they refinance later to secure better long-term terms.

Key Takeaways

Loan modification changes your existing mortgage

Refinancing replaces your mortgage with a new loan

Loan modification helps borrowers in financial hardship

Refinancing helps borrowers with good credit

Refinancing usually saves more money long-term

FAQs

Is loan modification better than refinancing? It depends on your situation. Modification is better if you have poor credit or face financial hardship. Refinancing is better if you have good credit and want long-term interest savings.

Does loan modification hurt your credit? Yes, it can. Lenders often require you to be behind on payments to qualify, which lowers your score. The modification itself might also be reported as a negative mark on your credit report.

Can you refinance after loan modification? Yes. If you get back on your feet, improve your credit, and make on-time payments for a certain period (usually 12 to 24 months), you can refinance your modified loan.

Which is cheaper: refinance or loan modification? Upfront, loan modification is cheaper because it has little to no closing costs. Long-term, refinancing is cheaper because it usually lowers your total interest rather than extending your loan term.

Final Verdict: Loan Modification vs Refinance

Deciding between a loan modification and a mortgage refinance comes down to a simple question: Are you trying to survive a financial crisis, or are you trying to optimize your healthy finances?

If you are struggling to make ends meet, behind on bills, and terrified of losing your home, a loan modification is your lifeline. It cuts the red tape and adjusts your monthly burden to something you can actually carry.

Understanding loan modification vs refinance helps homeowners make smarter financial decisions and choose the right option based on their situation.

If your income is stable, your credit is strong, and you just want to take advantage of better market rates, refinancing is the clear winner. It requires some cash upfront, but the long-term savings are incredibly powerful.

Evaluate your credit score, look honestly at your monthly budget, and reach out to your lender to explore your options. Taking action today is the best way to secure your home for tomorrow.

Sabir Abdirahman Mohamed is the founder of ThinkFixer and a personal finance and digital growth writer. He helps beginners learn how to save money, build online income streams, and grow blogs or businesses through practical SEO strategies. His content focuses on budgeting, smart money management, realistic ways to make money online, and step-by-step blogging guidance. His mission is to make financial and digital knowledge simple, actionable, and accessible for everyone.

")